Since day one, we've been dedicated to industry-leading transparency into our business processes and performance. Read through the following article and charts for monthly-updated insights into our book of business, as well as what we're seeing from a macroeconomic standpoint, and how we're changing our business to reflect that.

April's Performance

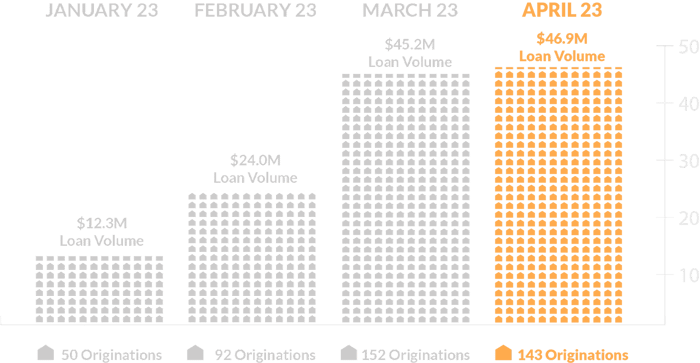

In April, we originated 143 loans, totaling more than $46.8 million in origination volume.

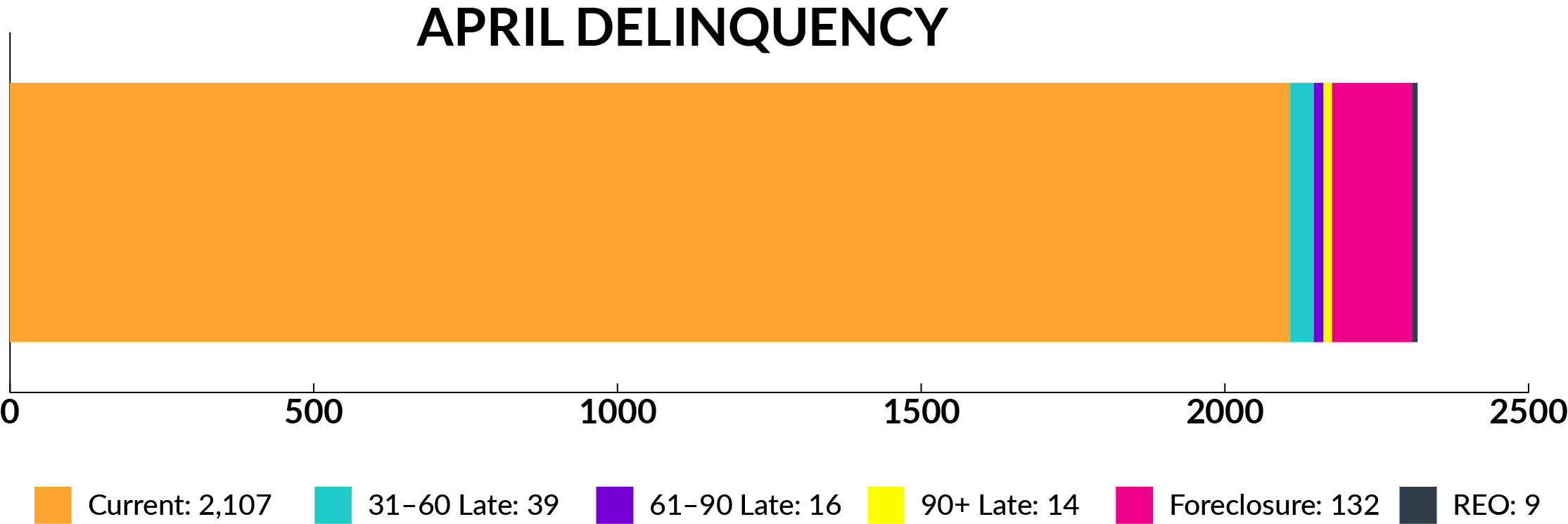

Additionally, as of May 1, 9.06% of our total loan count was 30 days or more late on payments.

Some things to pay attention to with the chart above:

- Month over month, fewer loans are falling into the 31-60 Days Late category.

- Additionally, fewer loans are being referred to foreclosure.

Because of these trends, and overall analysis of our book, and continued increases in origination volume, we feel confident we have reached a delinquency peak.

Investment Platform

Moreover, in the month of April we saw:

- $20.631M in new investments across all retail investment products (Borrower-Dependent Notes (BDN), PFNF, RBNF, and HRIF)

- 1,331 total investments

- 11.145% average rate of return

- $44,198,643.46 paid to investors, with a total of $5,008,820.85 in actual income, including:

- $4,651,265.86 in interest

- $15,248.68 in late fees

- $342,306.31 in extension fees

More Insight into Delinquencies

We are always focused on a successful exit to maximize the repayment of principal and speed to liquidity.

With foreclosures, unfortunately, we are at the mercy of county court systems working through lengthy foreclosure processes, or our borrowers exiting their projects. We know some of our delinquencies are strategic, as developers delay liquidity events of other projects for the 2023 buying season.

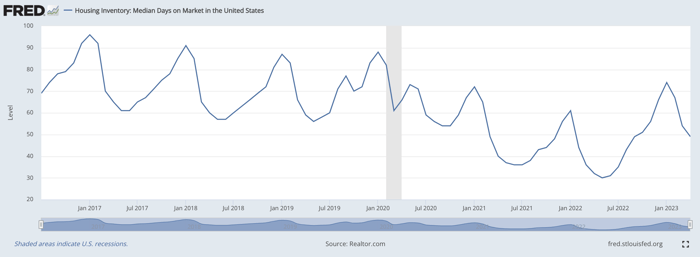

With the recent cooling of inflationary real estate figures, total days on market continues to come down to early 2022 levels, and home prices in most of our markets are continuing to climb back to mid-2022 numbers. This is in line with our thesis that — especially within our chosen operational geographies — there is a true housing supply shortage as household formations continue to significantly outpace housing inventory.

Housing Inventory Median Days on Market in the U.S.

Other things affecting the performance of our book include:

- Changing availability and/or terms of capital for refinancing or end-buyer financing impacts exit timelines and monthly payments.

- Several high-dollar loans remain delinquent on payments (with priority on exit and repayment).

- Continued supply chain issues and labor shortages contribute to construction delays and eventually, delinquencies.

How We Present Our Data

As you can see in the charts above, we show you the total count of delinquent loans. This is to remain transparent on our business performance, but also to better align with the Mortgage Bankers Association's (MBA) standard, published in its National Delinquency Survey (NDS), which is based on loan count. Additionally, the NDS states:

The delinquency rates and foreclosure starts rate are seasonally adjusted to account for trends in the data that are caused by the time of the year. For example, delinquencies tend to increase from the first to fourth quarters, peaking in the fourth quarter, before falling in the first quarter of the next year and beginning the cycle again."

The delinquency rates and foreclosure starts rate are seasonally adjusted to account for trends in the data that are caused by the time of the year. For example, delinquencies tend to increase from the first to fourth quarters, peaking in the fourth quarter, before falling in the first quarter of the next year and beginning the cycle again."

The data we share in our Performance Reports is not seasonally adjusted, but we feel it's pertinent to explain seasonal trends when applicable.

What We're Doing

As always, we're actively working with our borrowers to keep their projects moving forward, on track, and current on payments. We have recently restructured the lending side of our business in order to ensure portfolio performance is our top priority.

- Self-service tools to make it easier for borrowers to request draws, payoffs, and more.

- Our Account Management and Sales teams work closely with each other and borrowers to ensure payments and projects are current before proceeding with new loans for the same client.

- Additionally, the Account Management team works diligently to ensure as few loans as possible remain delinquent longer than 30 days.

- Updated, more efficient processes to review delinquent accounts and issue notice of default communications sooner.

We're also continuing to build a strong forward pipeline even in a somewhat uncertain real estate market, remaining selective on markets to enter and what projects we fund by focusing more on appraisals and historic performance. The Upright operational and business strategy is designed around utilizing a diverse capital stack so we're always positioned to weather market volatility and come out ahead.

If you have any questions or would like to provide feedback, email us at invest@upright.us. We will respond as soon as possible.

Log in to your account here, or start investing.